Updated June 2026

What Is Collision Coverage Insurance?

Collision coverage reimburses you for damage to your own vehicle after an accident involving another vehicle or a stationary object like a guardrail, tree, or mailbox. It also covers single-vehicle rollovers. Unlike liability insurance, which pays the other driver's expenses when you're at fault, collision pays your repair bill even when the accident is entirely your fault. You choose a deductible between $250 and $2,000 — the amount you pay out of pocket before the carrier writes a check for the balance.

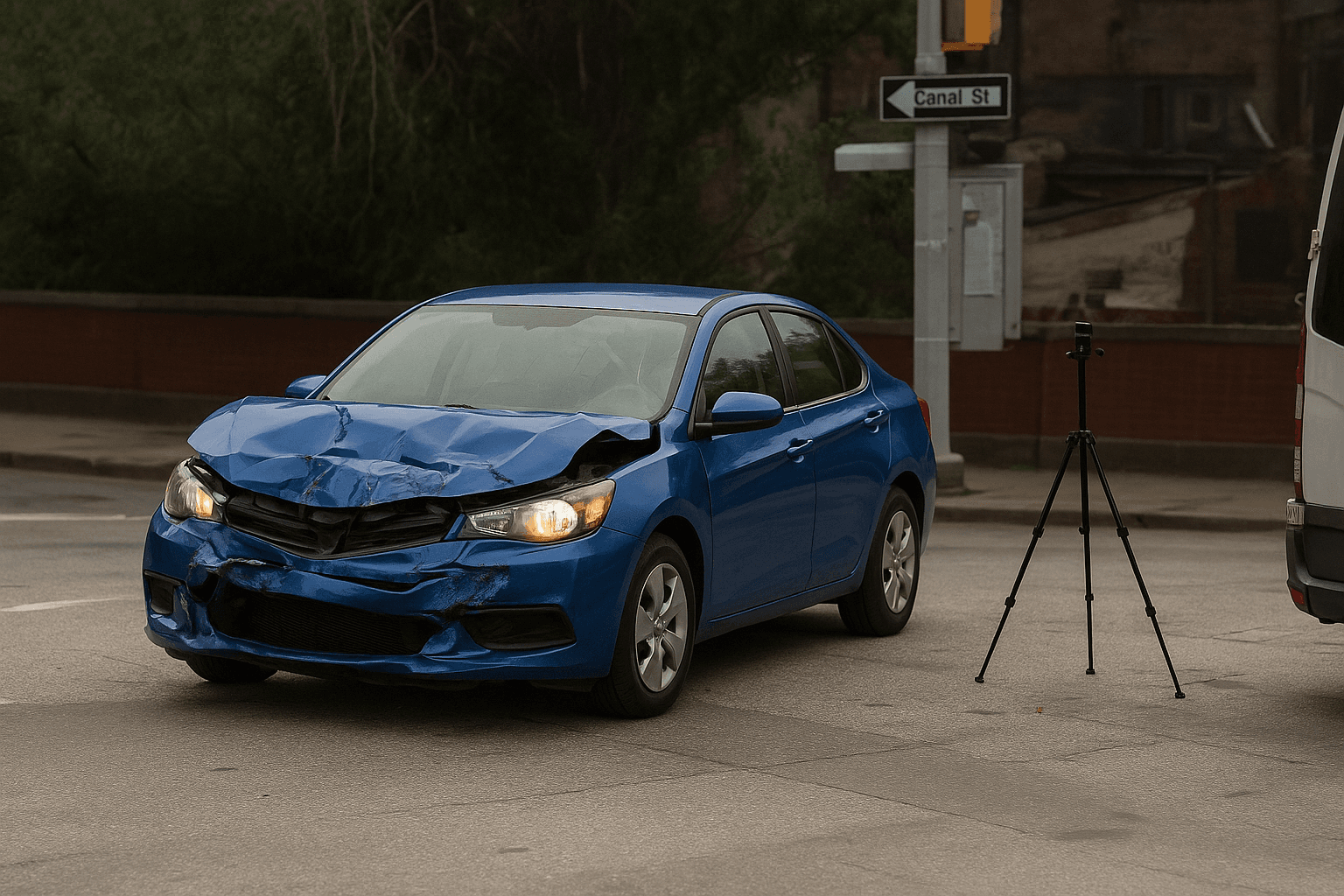

- You brake late at a stoplight and hit the car ahead. The other driver files a $6,200 claim for bumper and frame damage, and your own front end suffers $4,800 in damage. Your liability coverage pays the other driver's $6,200. Your collision coverage pays your $4,800 repair bill minus your $500 deductible, so the carrier sends the body shop $4,300 and you pay $500.

- An uninsured motorist runs a red light and totals your 2015 sedan valued at $7,400. North Carolina requires uninsured motorist property damage coverage, but the $25,000 per-accident minimum only pays if you don't carry collision. If you carry collision, it pays the claim first — your carrier writes you a check for $7,400 minus your $1,000 deductible, so you receive $6,400. Your carrier then pursues the at-fault driver to recover the payout, but reimbursement to you is not guaranteed.

- A deer jumps into the road, you swerve, and your car strikes a tree. The vehicle sustains $9,100 in frame and suspension damage. Hitting the deer itself would require comprehensive coverage, but hitting the tree falls under collision. Your carrier inspects the vehicle, determines it's repairable, and pays the $9,100 claim minus your $500 deductible. You pay $500; the carrier pays $8,600 to the repair facility.

Who Needs Collision Coverage Insurance?

Retirees carrying a loan or lease must maintain collision coverage until the balance is paid. If your vehicle is worth more than $8,000 and you lack the savings to replace it after a total loss, collision coverage spreads that risk across monthly premiums. Drivers with a history of at-fault accidents or those navigating high-density metro areas like Charlotte or Raleigh benefit from collision even on a paid-off car, because the likelihood of a future accident justifies the annual cost.

Calculate your vehicle's actual cash value using Kelley Blue Book or NADA, subtract your deductible, then divide the net payout by your annual collision premium. If the result is under three years, the coverage costs more than it's likely to return. Retirees with paid-off vehicles worth under $6,000 and clean records should compare the annual premium to their ability to self-insure — many find dropping collision and banking the savings delivers better financial outcomes over a five-year horizon.

How Much Does Collision Coverage Insurance Cost?

Collision coverage typically adds $33 to $75 per month ($400 to $900 annually) to a North Carolina retiree's premium, depending on the vehicle's age, value, and your ZIP code.

- Vehicle value — a $22,000 car costs more to insure for collision than a $6,000 car, because the maximum payout is higher.

- Deductible selection — choosing a $1,000 deductible instead of $500 reduces premium by 15 to 25 percent, but increases your out-of-pocket cost per claim.

- ZIP code — urban counties like Mecklenburg and Wake show higher collision rates than rural counties, raising premiums by 20 to 40 percent for identical coverage.

- Driving record — at-fault accidents in the past three years increase collision premium by 30 to 60 percent, even if the prior accident involved a different vehicle.

- Annual mileage — drivers logging under 5,000 miles per year qualify for low-mileage discounts with select carriers, reducing collision cost by 10 to 20 percent.

- Vehicle safety features — cars with automatic emergency braking, lane-departure warning, and blind-spot monitoring earn collision discounts of 5 to 15 percent from carriers that file those rating factors.